Baltic Sea to the Pacific Ocean, Russia has 22% of the world’s forest area (as defined by FAO – the most in the world. By comparison, the next largest forest countries are: Brazil with 16%, Canada 7% and U.S. 6 % of the world’s forest cover. The most often referred figure for Russia’s total forested area is 763.5 million hectares (equal to 1.87 billion acres). There is, however, some doubt about the origin and accuracy of this figure.

Basic statistical figures about the Russian Forest Fund for January 1993 (published in 1995) estimate forested lands. All figures are in thousands of hectares.

Statistics about the Russian Forest Fund and Rosleskhoz (State Forest Service) as of January 1993 (published 1995).

All figures in thousands of hectares.

total |

||||||

| Total Forest Fund area |

1180881.6

|

1110481.6

|

133092.0

|

977389.6

|

168170.5

|

809219.1

|

| Forest Lands area |

886538.4

|

825188.5

|

69968.1

|

755220.4

|

139124.1

|

616096.3

|

| Lands Covered by Forest |

763502.0

|

705789.2

|

50800.9

|

654988.3

|

132340.7

|

522647.6

|

| Young Forest Plantations |

3806.1

|

12.7

|

3793.4

|

2729.8

|

1063.6

|

|

| Seedling Planting Areas |

55.3

|

0.2

|

55.1

|

45.4

|

9.7

|

|

| Natural Rare-Standing Trees Areas |

115537.9

|

19154.3

|

41439.3

|

0.0

|

41439.3

|

|

| Lands Non-Covered by Forest |

54944.3

|

4008.2

|

50936.1

|

|||

| Non-Forest Lands area |

285293.1

|

63123.9

|

222169.2

|

29046.4

|

193122.8

|

Note: The category of Forest Fund lands temporary passed to other land-users does not exist in regulations any more. In Soviet times it meant the lands passed at no charge from the Forest Service to other state agencies. The biggest part of those 133 million hectares were passed to open pit mining enterprises and military structures. The status of these lands today is not clear.The figure of 763.5 million hectares is used to calculate the forestation (percentage of total country area covered by forests) for the Russian Federation at44.7%. The same figures for European and Asian parts of Russia are – according official statistics – 38.5% and 46.7%.

Clearly, though, Russia’s vast forests are a natural resource of global importance, both ecologically and economically. The forests already serve Russia and the rest of the world as a source of timber, as a symbol for wilderness and as a critical stabiliser of the global climate. According to recent estimates by the World Resource Institute, about 26% of the world’s last frontier forests are in Russia. Careless exploitation of Russian forests could hold back Russia’s economic renewal, permanently degrading the local environment and destabilizing the global climate.

Over 11,000 species of vascular plants (of which 461 are classified as endangered by the Red Data Book, but some 2000-3000 are estimated as being under threat), 320 mammals (64 endangered), about 730 birds (109 endangered), 75 reptiles (11 endangered), about 30 amphibians (4 endangered) and 270 fresh-water fish (9 endangered) species may be found in Russia. This constitutes about 8% of global vascular plant flora, 7% of the mammal fauna and almost 8% of the bird fauna.

In spite of a long history of economic development, the lands of Northern Eurasia are relatively little disturbed, especially in Siberia and the Far East. Industrial and agricultural expansion into these regions has been difficult due to permafrost, the cold climate and land which is difficult to cultivate. The worst decline in biological and landscape diversity has occurred in Northern Caucasia, in the Volga Region, in Central European Russia and in Southern Siberia.

The other regions have experienced mostly local human impacts, and almost 90% of tundra, up to 70-75% of taiga forests and 20-30% of Asian steppes have remained close to their natural state.

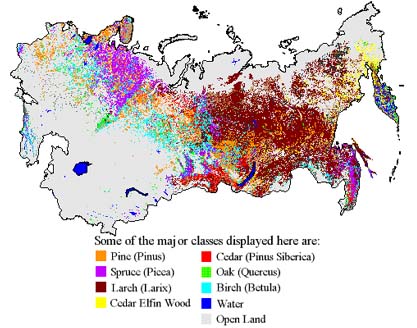

Forest Cover Map of the Former Soviet Union

Somewhat more than half the forests are young forests greatly altered by man, whereas less than 15% can still be classified as frontier forests (large virgin forests). The other forests consist of fragments of old-growth and other mature forests and areas dominated by marsh-bog complexes. In the central and especially the southern taiga zones, the situation differs greatly from that in the Northwest of Russia. These regions have a long history of quite intensive land use, and large untouched areas are rare or absent. In spite of this, much valuable nature exists in these areas as well.

Compared with similar vegetation zones in Scandinavia, for instance, the Russian zones are found to still have a relatively high proportion of patches close to their natural state. Natural restoration of forest is much quicker in the south than in the north. It is also self-evident that the species diversity is much higher here. The Russian zones, although not totally untouched, are of the highest quality that exists, and there is no question about the value of these sites. The Karelian Isthmus region in the Leningrad Oblast is a good example of this.

Areas untouched by man are rarer than in the Republic of Karelia, but in comparison to Southern Finland, the Karelian Isthmus is a nature paradise. There are still considerable areas where human influence is slight, and many natural values are present, e.g. areas with a diverse flora, rich in herbs; broad-leaf forests; lakes and marshy areas of ornithological value with resting places for migrating birds; esker areas valuable for their flora and geomorphology; and representative rock areas.

Despite the relative richness of the natural forests in European Russia, the taiga as a whole is relatively fragmented and disturbed by various human activities, including forestry. Few substantial areas of unfragmented natural forest remain. The remaining areas include the Pechora Ylych region and its headwaters in the Republic of Komi, the forests along the Karelia-Arkhangelsk and Arkhangelsk-Komi borders, the subtundra forests in the Arkhangelsk, Komi and Yamal-Nenets autonomous regions and the eastern part of the Kola peninsula, the montane forests along the Swedish-Norwegian border and the so-called Green Belt along the Finnish-Russian (Karelian) border.

The forests of the Green Belt are one of the most important boreal biodiversity centres in Europe as they connect the continental Russian taiga to the more oceanic boreal forests of Fennoscandia. Without this ecological bridge the forests of Scandinavia would become isolated from their genetic mainland.

Many species in the Red Data Books (endangered lists) for Sweden and Finland still exist in viable populations in the Northwest of Russia. The main reason is that the forests, although intensively used or disturbed in many places, have not been subject to the same systematic and intensive forestry methods applied in neighbouring Finland and Sweden.

Forestry in Russia

The annual growth of the Russian forests is nearly 1000 million m3 . However, much of this potential cannot be used even in principle by the forest industry due to environmental constraints, the remoteness of forests from domestic and international markets, the absence of a transportation network and technological limitations.

It has been estimated that the economically exploitable forests comprise 55% of the forested areas under state forest management. Mortality amounts to 49% of the gross growth. This is an extremely high figure compared with most other countries. This is due to the fact, that there are still huge areas in Russia with unexploited old-growth forests, as well as a significant amount of forest fires, insect outbreaks etc. The high figure for mortality demonstrates a special feature of Russian forests, namely that large areas are still unmanaged and thus to environmentalists appear undamaged by man. Similar, sizeable areas have nearly disappeared from Scandinavia, where “ecological forest management” has now been developed to restore some of the original features of the forests.

From the environmental point of view, until 1996 the situation regarding old-growth forest loggings was chaotic. Even amongst environmental organisations and researchers there was no consensus on the locations and relative values of old-growth forests. Virgin forest areas previously almost untouched by man were destroyed at an increasing rate in large- scale clear cuttings. The environmental organisations followed the situation actively in some key areas, but they lacked the means to influence the general situation.

New enterprises and forest industry

The new owners of Russia’s forestry enterprises are largely managers from the old era who consider their new possessions to be like the collective farms of the past. They do not attempt to gain profits for the firms, but rather to maximize personal wealth. These owners, former officials and managers, have privatized the industry into their own hands, selling off assets rather than building up new ones, and exporting capital instead of creating new capital.

Timber harvesting enterprises can obtain harvesting options by leasing forest areas for periods of 1-49 years or by purchasing the harvesting rights to a single forest stand. Forest resources are mainly allocated on the basis of long-term leasing. Priority in forest resource utilisation is given to logging enterprises which have operated in a particular territory for a long time and which have appropriate capacity for logging and processing of the wood and other forest products, as well as to enterprises supplying forest industry products for domestic demand.

Russian forestry employment and social aspects

The Russian forest sector is a significant employer that directly accounted for more than two million employees in Russia in 1990. Between 1990 and the mid-1990s the number of people directly employed by the forest sector fell from 2.0 to 1.8 million people. Employment in the forest sector has not fallen as steeply as the physical output.

Forestry in northwestern Russia is characterised by a relatively low proportion of forestry workers to the total number of staff, while the proportion of manual workers in the forest industries, as well as on the subsidiary agricultural farms and in the exploitation of non-timber forest products, is about 45% of all employees (the proportion of persons in charge and specialists being 25%).

The proportion of forestry workers is only 5-6%, while 15-16% are persons in charge and specialists, and 20-25% are forest-guard personnel. State forest enterprises had a wide social importance in Soviet society; they provided employment, produced goods and services, and offered a large variety of social facilities for employees and the local population. The transition to a market economy has forced firms to be much more efficient economically. With no subsidies, firms have been forced to substantially downsize social functions.

Forest governance, institutions and official management

The Federal Forest Service of Russia manages about 94% of the total forest land area in Russia, with another 4% belonging to agricultural organisations, 1% to the Committee of Environment Protection and 1% to other state bodies.

The Basic Forest Law of the Russian Federation was issued in 1993, to be replaced in 1997 by the new Forest Code. The reform of 1993 enabled some progress to be made towards establishing market relations. According to the Basic Forest Law, forest leasing and auctions of standing timber were allowed, and forest leasing is the main element of market relations. Any person (including a foreigner) can be a leaseholder.

Forest lease relations have been introduced in Siberia, the Far East, Urals and in the North and Northwest of the European part of the Russian Federation. In such regions as Arkhangelsk, Vologda, Kostroma, Primorsk and Khabarovsk, practically all economically accessible and profitable forests have been given to leaseholders. According to the new Forest Code, the right to grant licences belongs to the regional authorities.

The licences are granted by direct negotiation, auction or tender, often in a non-transparent way. At present, leaseholders have at their disposal forest tracts with an allowable annual cut of 85 million m3, approximately 75% of the average actual volume of cuttings during the past two years. The leaseholders are typically formerly state-owned logging companies. This has been accompanied by the development of stumpage auctions. Auctions have made it possible to establish real prices for standing timber, but still in 1996 only 1.7% of the total timber volume was sold through auction.

Many of the newly passed regulations do not take into account the rich diversity of Russia, and the same rules are applied to widely different forest and landscape types which again results in lack of compliance. In addition, the powers and responsibilities of federal, state and local governments are not clearly drawn up. This leads to conflicting regulations passed by federal and regional legislatures.

Currently the Federal Forest Service has a double role in Russian forestry. In addition to managing nearly all Russian forests, it is also responsible for about 20% of the logging, through intermediate and sanitary loggings. According to Greenpeace Russia, the Federal Forest Service has thus been transformed from an independent controller of forestry to a competitor of the forestry companies, leading to serious problems in the control of forestry and the development of federal forest policy.

Another problem is caused by the non-transparent information policy of the Federal Forest Service. As no detailed information about forestry is publicly available, verification of the actions and claims of forest authorities is not possible. For example, the official figure for the proportion of areas reforested after clear-cutting is 40%. However, samples studied by Greenpeace Russia showed that the correct estimate is roughly 2%.

Other problems stem from confused and incompatible classes of forest and official statistics. The term “Forest Fund” in the Russian forest management system originally it just meant all forest and related lands under governmental jurisdiction. Because all forests (as with all other lands and resources) were state-owned in the former Soviet Union, the Forest Fund theoretically included all Russian forests. The dominant part of the Forest Fund was (and still is) under management of Russian Federal Forest Service (Rosleskhoz). However, some parts of the Forest Fund were (and still are) managed by other structures and agencies.

Very often under the Forest Fund, authorities mean only that part of it which belongs to the forest service, Rosleskhoz. In the official forest statistic published in 1995, are two different tables with different total figures in columns both entitled: “The total area of the Forest Fund lands.” (One figure is about Forest Fund under the Rosleskhoz jurisdiction, another one about whole Forest Fund area.)

The new Forest Code of 1997, the current federal-level act on forests and forest sector, makes the situation more complicated: two categories of forests (forests on military lands and city forests) were excluded from the Forest Fund but still stayed state-owned. The Forest Code introduces the special term for these forests: “Forests Not Belonging to Forest Fund.”

Added into the Forest Code is one more categorization of forest: “tree-bushy vegetation,” situated on other land categories such as town land, some agricultural lands, Water Fund lands, transportation lands and some others. This means different pieces of forest on the same type of land may belong to different categories.

For example, the “tree-bushy vegetation” in towns (trees around houses, along streets etc.) is different from “city forests” (which are usually represented by large city parks) which belong to “Forests Not Belonging to Forest Fund” classification. Also, in agricultural lands you could find both Forest Fund forests (the largest part of them) and some “tree-bushy vegetation.” The reasons to classifying particular forest as one of the categories are mainly historical or sometimes just random.

Nature Conservation Efforts A system of protected natural areas encompassing all natural zones and principal mountain massifs has been developed in Russia in over the past 80 years. At present, the Russian Federation has 99 state zapovedniks, i.e. strict scientific nature reserves, which meet the category I criteria of the IUCN classification of protected areas. The total area of the zapovedniks is 33.2 million ha, of which 26.7 million ha (1.56% of Russia’s territory) is terrestrial area. At present, Russia has 34 national parks, 2/3 of which have been established during the preceding six years. The total area of the national parks is 6.8 million ha (0.40% of Russia’s territory). There are plans to establish some 40 additional zapovedniks and parks.

Practically all the national parks are located in forest fund areas and are managed by the state forestry authorities. In addition, the Russian Federation has 52.2 million ha of zakazniks with either regional or federal status. The protective regime of zakazniks is very broad – from category I to category VII of the IUCN classification. Thus it should be noted that most of the zakazniks, especially the game reserves, do not support forest protection.

There are even many zakazniks in which hunting is not allowed but clear cutting is. The total protected area is about 5% of the forest resource area in Russia, but only about 2% is strictly protected. Thus, more protected areas giving better coverage are required to maintain biodiversity.

The Russian forests have been divided into three categories with respect to their economic and ecological characteristics. The first category comprises forests with a protective function, e.g. forests along watersheds. However, these forests, comprising some 20% of the forested land, are certainly not strictly protected. According to Greenpeace Russia, intensive intermediate and sanitary tree fellings are practised in 95% of these forests, and even clear-cutting (maximum size 10 hectares) is allowed in 50% of the area.

The second category includes forests in populated areas and forests with low timber production, comprising 5.5% of the total area. The vast majority of forests, 74.5%, is included in category three, industrially exploitable forests, where clear-cutting (maximum size 50 ha) is the main forestry practice.

Environmental regulations Efforts

Russia has made a number of international environmental commitments with respect to forestry. Due to a weak national forest management policy, Russia has difficulties fulfilling these commitments. The inefficiency of environmental control resulting from a lack of resources and inefficient organisations is well-documented. Russian authorities are too weak to ensure compliance with environmental legislation, and adequate mechanisms and institutions for effective implementation are simply absent. Violations of environmental regulations are commonplace.

Lack of compliance with, and implementation and enforcement of environmental standards can be traced to three related factors:

- the legislative process, which allows little dialogue with stakeholders and thus builds little political will for implementation;

- the institutional structures responsible for implementation and enforcement, which have limited resources and ambiguous mandates;

- the substantive standards themselves, which are sometimes unrealistic and frequently unclear.

Expectations that a drastic drop in industrial production in Russia would bring about corresponding reductions in pollution and contamination have not been realized. In reality, these problems are as acute now as before the transition. This can be explained by obsolete industrial technology, lack of investment in environmental protection, and other factors that keep pollution levels substantially higher in Russia than in the West. Annual national Russian reports on the environmental status support this conclusion.

Impact on old-growth forests and biodiversity

Wood harvesting has changed the age structure of the forests in the European part of Russia dramatically during past decades. The area covered by mature and over-mature forests has decreased from 51% in 1966 to 38% in 1993. The proportion of mature and over-mature stands in the European part of Russia is only 19% of the figure for the whole country, while this region produces 57% of the annual harvest.

However, the old-growth forests of the European part of Russia are still a world-class natural heritage and the evaluation of their importance should be done in this light. The conservation of old-growth forests is not included in Russian forest legislation in any way, even in the areas where the remaining old-growth comprises only a small fraction of the total.

Thus the major part of the remaining old-growth areas in the Northwest of Russia are still under acute threat, and the remaining area is getting smaller every year. The possible introduction of “softer” logging technologies will not solve the problem, as the only way to maintain the functional characteristics of old-growth areas is by protection of sufficiently large non-fragmented areas.

European and other international environmental funding should urgently be directed to the protection of these forests. Biodiversity conservation efforts in protected areas are fundamentally important, but a full program of forest biodiversity conservation must also deal with forests subjected to timber harvesting and other human intervention.

Forestry practices should be developed in more ecological direction – e.g. by leaving patches of mature and dead trees when harvesting, regenerating with mixed species and refraining from clear-cutting, especially in all-aged stands of shade-tolerant species.

In future, consumer demand for sustainable forestry and the application of more ecological technology in forest production will require the adoption of a new approach in nature conservation, timber harvesting, forest industries and in marketing. The moratorium on logging of old-growth forests (to which a major part of Finnish companies have committed themselves) may be seen as the first step in this direction.

However, in most cases, the Russians’ own timber harvesting enterprises are poorly prepared to meet the ecological demands.

Russia’s old-growth forests and conservation efforts

Old-growth forest protection has always been one of the priorities of the Russian conservation movement. However, it is difficult to protect them without knowing where they are located. In many cases the lack of information about old-growth location resulted in leaving the most valuable forests unprotected, while protection status was applied to less valuable forest areas or even only to those ones which timber companies have voluntarily agreed to leave for conservation. The last option has not led to adequate biodiversity conservation. Information about old-growth location is also important for timber companies, which would like to avoid environmental conflicts and introduce environmentally responsible forestry.

Here are some successful attempts to apply analyses to identify relatively undisturbed Russian forest ecosystems:

Sikhote-Alin’, Russian Far East

– An ongoing mapping project by Biodiversity Conservation Centre and Socio-Ecological Union.

Novosibirsk oblast’

– An ongoing project for mapping valuable forests in a few districts of Novosibirsk oblast’, Western Siberia. The project of Ecological Club of Novosibirsk State University.

European Russian North

– The mapping of only the largest (more them 100 thousand hectares) areas of little-disturbed forest in European Russia. Made by the Forest Club organizations (Biodiversity Conservation Centre, Greenpeace Russia, Socio-Ecological Union) in 1999. The following regions are covered: Murmansk oblast’, Arkhangelsk oblast’, Vologda oblast’, Perm’ oblast’, Karelia Republic, Komi Republic and Komi-Permjatsky.

The Last Frontier Forests Report

– issued by World Resources Institute in 1997. The report also covers the whole of Russia.

Karelia Republic

– The kvartals (forest blocks) level based map of potential old-growth forests areas in the Republic. Prepared in 1996 jointly by Biodiversity Conservation Centre and Greenpeace Russia. Last updated in spring 1999. This map is the base for still on-going logging moratorium announced by a few largest forest companies. Some more earlier historical examples also include:

1984-87 – Analysis of the little-disturbed forests remained in Nizhny Novgorod Region conducted by the Druzhina (Student Corps) for Nature Conservation of Nizhny. This analysis became the basis of the entire program of biodiversity conservation and protected areas networking in the region. 1980s to early 1990s – Search for intact plots of broad-leaved forests in European Russia by a team of the scientists from different institutions. One of the results of this work was the creation of the Kaluzhskie Zaseki (abatis lines) Zapovednik (in Kaluga Region), which preserves a unique tract of little-disturbed broad-leaved forests.

Wood harvesting in Russia

The annual allowable cut (AAC) is set by the Federal Forest Service of Russia (Rosleshos). The AACs only consider final felling and commercial wood (industrial wood and fuelwood) in forests under state forest management. The Russian AAC excludes thinnings. The AAC is based on the status of the forest inventory, forest regulation and silvicultural handbooks. The development of the Russian AAC is shown below:

Fig 2Russian Annual Allowable Cuts, 1965-1997 [in million cubic metres]

However, the methods of calculating allowable cutting levels are in many cases old- fashioned and result in unrealistically high figures. Quite apart from ecological sustainability, even economically sustainable utilization, with a harvest equal to the annual net growth, is rarely used. A common method of calculating the AAC (e.g. in Karelia) is to divide the amount of advanced, mature and overmature forests by the number 60.

However, as the rotation period for pine is 120 years, the AAC thus obtained is well above even the economically sustainable level. This tradition for calculating the AAC originates from the Soviet era, when the lespromkhozes were intended to operate for a period of 20-30 years only. Still continuing their operation, many lespromkhozes suffer from a shortage of raw-material as they already have used a major part of their forest stock during the past decades.

In addition, the data on which the planning is based is often inaccurate. Thus, often the planned harvest level cannot be realized, resulting not only in economic but also ecological problems. Attempts to realize the overestimated AAC often lead to logging of old-growth forests, as the volume of growing stock per hectare is greatest there. The annual level of realized industrial loggings increased from 150 million m3 in 1946 to a maximum of 350 million in the late 1960s, before falling below 100 million m3 in the 1990s – a dramatic decrease in the annual level.

The Federal Forest Service estimates that the grey economy accounts for around 10% of the total wood volume. However, some scientists claim that in reality harvest levels may be 1.5-2.0 times higher than the official estimate, due to the shadow economy, intentional underestimates of production to evade taxes and shortcomings in compiling the statistics.

Fig 3Estimated total timber harvest in Russia, 1989-1997 [in million cubic metres]

This table gives an example of such estimates. The flow of wood to the grey economy is not taken into account when planning the AAC. There are also substantial losses of wood in the process from felling to final product. Losses are estimated to be on average 20% of the gross harvest.

Overharvesting by clear-cutting (which the authorities have accepted for several decades) has led to the depletion of forests in the European part of Russia, worsening the ecological conditions over vast areas. It has also resulted in the loss of highly productive sites. This development has ultimately resulted in a decreased supply of wood to industry.

The over-harvested areas in European Russia have a low potential for increased production. The resources have been exploited in a very unsustainable manner. The most productive coniferous stands have been exploited, while the less productive ones and stands of deciduous species have hardly been used at all.

As a result, huge areas of soft deciduous secondary forests have been generated and there has been a steady increase in swampy forests of lower site classes. By 1990, for example, the growing stock of mature forest could provide for harvesting (at 1990 levels) for 25 years in the Vologda Oblast, for 36 years in Karelia, and for 40-45 years in the Murmansk oblast. Thus, even though only 82% of the total AAC was harvested between 1970 and 1990 in European Russia, the AACs were violated for individual tree species and species groups, and at subregional level.

Prices and costs of Russian forestry

The price of wood in Russia is extremely low compared to EU countries. Low prices cause problems, because they mean also low budgets for introducing sustainable forestry and for forest protection and preservation.

In Karelia, for example, one cubic metre of best quality saw-timber pine, situated at most 10 kilometres from transportation facilities (such as a railway station), in 1998 cost less than 10 Finmarks (FIM), whereas the average price in Finland was 275 FIM. The stumpage payment, averaged over all wood sold in Russia, was less than 4 FIM at the end of 1998. Furthermore, for sanitary and intermediate fellings there is no stumpage fee at all.

This has lead to a situation where sanitary and intermediate fellings are commonly used as a tool for economic exploitation. The sharp cut in budgetary allocations for forest management, including expenditure on protection, conservation and reforestation, as well as on scientific research, has serious effects on the possibilities for sustainable forestry and nature conservation. According to some sources, forest supervisors, for example, have been receiving as little as 10% of the required funding. In many cases, the forest service has only enough money to retain its employees and no money is left over for fighting forest fires, enforcing logging regulations, and making periodic inventories.

In the absence of federal and state funding, local forest service supervisors have to rely entirely on stumpage fees and fines paid by logging companies.

The very important question is to whom the benefit from forestry goes. By law, 40% of stumpage fees and payments for leases are directed to the federal budget, and the remaining 60% to the budgets of the members of the Russian Federation. However, as the stumpage fees are extremely low, it is clear that there is a lot of loose money involved. The distribution of this money among domestic and foreign forestry companies, various middlemen and other parties is totally unclear. It has been estimated that in the case of wood exported to Finland some 60% of the money is linked to corruption.

Fig 4 Exports of forest industry products from Russia in 1997.

Swedish and Finnish involvement in Russian forestry

The total Swedish import of timber and wood products from all countries was more than 11 million m3 in 1999 and this is expected to rise in 2000. The imports of timber to Sweden from Russia and the Baltic countries have increased by 70% between 1995 and 1999. Total imports from Russia and the Baltic countries in 1999 were more than 9 million m 3 . This accounts for more than 80% of the total import for timber and wood products to Sweden.

A survey of the major players was carried out in August and September 2000. Those in the trade can be divided into four main categories: forest industry corporations, independent sawmills, forest owners associations, and import agents. Of these, the biggest players are the import agents and the forest industry corporations.

The import agents responding to the study reported imports of almost 4.1 million m3 annually from Russia and the Baltics. The forest industry companies responding reported imports of almost 7 million m3 . The independent sawmills reported almost 1.1 million m coming from Russia and the Baltics. The central and southern sawmills are the predominant importers within the independent sawmill industry.

The forest owners associations, with the exception of SÖDRA, which is importing over 1.4 million m 3 from Russia and the Baltics, are minor actors in the trade. All respondents importing timber and wood products who were not classified as import agents were buying some timber through import agents either in Russia or in the Baltics or both.

The larger import agents, Lemo Agencies AB and Thomesto Sverige AB have their own logging and wood procurement companies in Russia and the Baltics respectively. Many of the forest industry corporations have set up their own wood procurement companies in the Baltic countries. Korsnäs, Holmen, and StoraEnso, in addition to wood procurement companies also have logging companies in the Baltics. The independent sawmills are importing through import agents and the forest industry corporations or SÖDRA .

Increasingly in Sweden many small independent sawmills are consolidating their wood procurement into single larger wood procurement companies. Some of these companies are relatively large importers of timber from Russia and the Baltics.

The number of actors, especially middlemen involved in the trade seems to have decreased over the last three years. The nature of the involvement on the ground in Russia and the Baltics has changed. Swedish companies, many of which were setting up logging or forest industry operations on the ground in Russia have almost entirely pulled out of Russia and now concentrate on imports of roundwood through the import agents.

At the same time the Swedish forest industry corporations along with SÖDRA and the import agent, Thomesto Sverige AB have established themselves on the ground in the Baltics, primarily in Estonia and Latvia.

Vologda and Leningrad Oblasts in Russia are the central source of timber for the Swedish market. Smaller quantities of timber are also imported from the Russian regions of Novgorod, Pskov, Komi, Archangelsk, Tver, and Karelia.

Of the Baltic States, Latvia is the largest supplier of timber and wood products (3.4 million in m3 in 1999 followed by Estonia, (2.2 million m3 in 1999). The trade with Lithuania was less than 500,000 m 3 in 1999. The source of the Swedish import from the Baltic States does not seem to be concentrated in any specific regions in the respective countries.

Some companies seem to have very limited or no knowledge about the origin of their imports. They do however seem to represent a relatively small proportion of the overall trade. In the Swedish offices of the companies contacted there seemed to be very little knowledge, if any about the qualities of the forests from which the timber is coming and the ecological and social impact of the forest practices, both in the Baltics and Russia.

Companies attempting to gain knowledge about the origin and impact of their imports are using a number of mechanisms. Many rely on the trustworthiness of the standard and enforcement of national forest management legislation and controls to ensure responsible trade. This may be a successful strategy if forestry legislation is appropriate and enforced. However, NGOs on the ground in both Russia and the Baltic countries question the trustworthiness of the standard and enforcement of state legislation and controls.

Some companies have developed specific tracking systems down to the harvesting area. Other companies employ mechanisms such as site visits, written contracts, limiting the number of suppliers, cooperation with environ-mental organizations, education of local partners and workers in Swedish standards for environmental forest management, using local logging companies, and participating in certification processes to increase control of their imports.

Swedish companies may play an important role in speeding up the development of certification, by taking an active part in standard development processes in cooperation with national stake-holders and by demanding certified raw materials. Companies, which have not yet reached the first level of knowledge about the origin of their imports, urgently need to do so in order to move towards a more responsible trade.

Finnish forestry companies in Russia

The wood trade from Russia to Finland has a long history. Already in the beginning of the 1970s, Finland imported some 5 million m3 of wood from Russia, roughly half the current amount. Imports remained at approximately the same level until the early 1990’s, when they rose rapidly to the present level.

The number of Finnish companies involved in Russian forestry is large – it is estimated that at least 100 companies are involved in one way or another. There are, however, large differences in scale, location and type of operation. Most of the companies involved are quite small. Less than 10 companies procure more than 100,000 m3 timber per company from Russia annually.

The main reasons for the increased imports are the poor condition of Russia’s domestic forest industry and the increased demand, especially for birch pulp, in Finland. Low wood prices combined with a highly corrupt timber trade system have also attracted some companies and certain so-called middlemen looking for opportunities to make a quick profit.

From the Finnish point of view, the Russian forests serve as a mainland providing a continuous supply of a number species specialised in old-growth forests living in the fragmented Finnish old-growth forest patches. This conclusion is supported by maps indicating observations of species specialised in old-growth forests. The species increase near the Russian border more than would be expected from the relatively high proportion of old-growth forests in the region.

The environmental policies of Finnish companies concerning operations in the Northwest of Russia have improved considerably during the last few years. The existing moratorium commitments of the major companies are credible verification that the companies will not participate in the destruction of old-growth forests in Karelia and Murmansk. Furthermore, there is some hope that this commitment will in future comprise the whole of northwestern Russia.

It can even be argued that the Finnish companies are applying their best environmental policies in northwestern Russia. In Finland, a similar moratorium for old-growth forests has been demanded by the environmental organisations for several years without a positive response.

In addition to the moratorium, another positive aspect of the operations of Finnish companies in Northwest Russia has been the transparency of their information policy. Nevertheless, the situation in the Northwest of Russia is far from satisfactory. In the more remote areas, where wood is mainly logged by local forestry companies and then transported by train to Finland, the main problem is still the logging of old-growth forests.

After the extension of the moratorium hopefully this will be solved, but the problem of the methodology used will remain. Large-scale clear cutting, devastating vast areas for a long time, can certainly not be considered environmentally sound. Even in areas close to Finland, there are still some Finnish contractors logging inside the moratorium areas. Furthermore, from a social point of view, the structural problem of the wood trade still remains unsolved. Clear-cut logging by Finnish companies using Finnish machinery and Finnish employees leaves very little for the local communities. Export of roundwood should rather be replaced by developing further processing at the local level.

In the Leningrad Oblast the situation is especially unclear. A recent study by a local non-governmental organisation (The St. Petersburg Society of Greenpeace Supporters 1998), as well as a study by a mixed commission for auditing the state of forestry (Greenpeace and Biodiversity Conservation Centre 1997) reveals that a large proportion of the logging and wood trade in the region is illegal.

Finnish companies are the main purchasers of wood from this region, having recently rented large areas for several decades. A moratorium map for the Leningrad Oblast, which will hopefully offer a partial solution, is urgently required. As a first step in this direction, the St. Petersburg and Finnish non-governmental organisations have prepared a preliminary map of valuable areas in the Karelian Isthmus.